The landscape of American healthcare is undergoing a significant shift as specialized providers move to address the unique needs of the growing "business of one" demographic. Solo Health Collective has emerged as a prominent alternative to the traditional Affordable Care Act (ACA) marketplace, utilizing a captive insurance model designed specifically for freelancers, consultants, and independent contractors. By pooling the collective buying power of self-employed individuals, the organization seeks to mitigate the high premiums and administrative complexities that have historically burdened the independent workforce.

The Growing Crisis of Freelance Healthcare Access

The rise of the "gig economy" has transformed the United States labor market, with recent data from Upwork and MBO Partners indicating that over 64 million Americans—approximately 38% of the workforce—performed freelance work in the past year. Despite the economic contribution of this sector, health insurance remains a primary structural barrier to sustainable self-employment.

Under the current framework, most self-employed individuals rely on the federal or state-level ACA marketplaces. While these exchanges provide essential protections, such as guaranteed issue regardless of pre-existing conditions, they are often characterized by high deductibles and rising monthly premiums. For many solopreneurs, the "Silver" and "Bronze" tier plans frequently result in "underinsurance," where individuals pay significant monthly costs for plans that require thousands of dollars in out-of-pocket spending before coverage begins.

Solo Health Collective was developed as a direct response to these market inefficiencies, aiming to provide a middle-ground solution for generally healthy independent workers who do not qualify for significant government subsidies but find traditional private insurance cost-prohibitive.

The Captive Insurance Mechanism: A Technical Overview

At the core of the Solo Health Collective offering is the captive insurance model. In a traditional insurance arrangement, a policyholder pays premiums to a commercial carrier. The carrier assumes the risk, manages the claims, and retains any surplus as profit. In contrast, a captive model allows a specific group—in this case, a collective of solopreneurs—to essentially fund their own insurance pool.

This structure mimics the self-funded insurance plans utilized by large corporations. By bringing together thousands of "businesses of one," Solo Health Collective creates the scale necessary to negotiate favorable rates with provider networks and pharmacy benefit managers. Because the collective is designed to be self-sustaining rather than profit-maximized for external shareholders, the model allows for more transparent pricing and lower administrative overhead.

The plan is managed by Health Business Group (HBG), an organization founded in 2015 that specializes in alternative health funding strategies. The Solo-specific initiative was launched in 2022 to refine these corporate-level strategies for the individual freelancer.

Chronology of Development and Market Entry

The evolution of Solo Health Collective follows a decade of fluctuating stability in the individual insurance market:

- 2010–2014: The passage and implementation of the Affordable Care Act (ACA) eliminated medical underwriting but led to a consolidation of provider networks.

- 2015: Health Business Group (HBG) is established, focusing on helping small to mid-sized businesses escape the traditional "fully insured" market through self-funding and captive models.

- 2018–2020: The Department of Labor attempted to expand Association Health Plans (AHPs), though legal challenges limited their widespread adoption for individual solopreneurs.

- 2021: Market research identified a "coverage gap" for self-employed individuals who earned too much for ACA subsidies but found the unsubsidized premiums of PPO plans reached upwards of $600–$800 per month for individuals.

- 2022: Solo Health Collective is officially launched, integrating a nationwide PPO network with the captive funding model.

- 2024–2025: The organization expanded its digital "concierge" infrastructure, moving away from traditional call centers toward a mobile-first, text-based support system to align with the workflow of modern digital nomads and freelancers.

Plan Specifications and Network Access

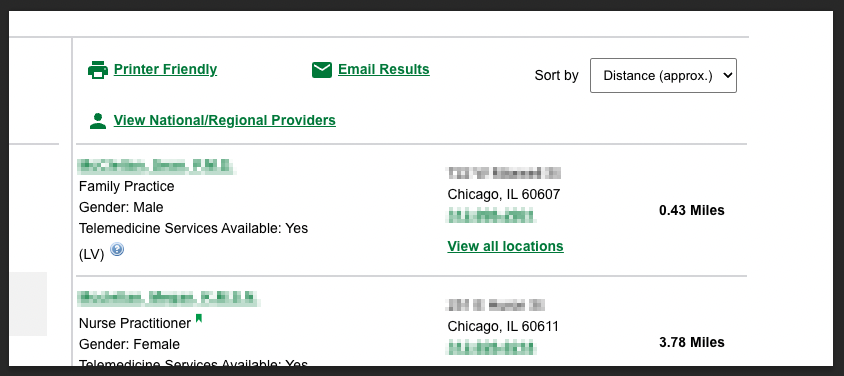

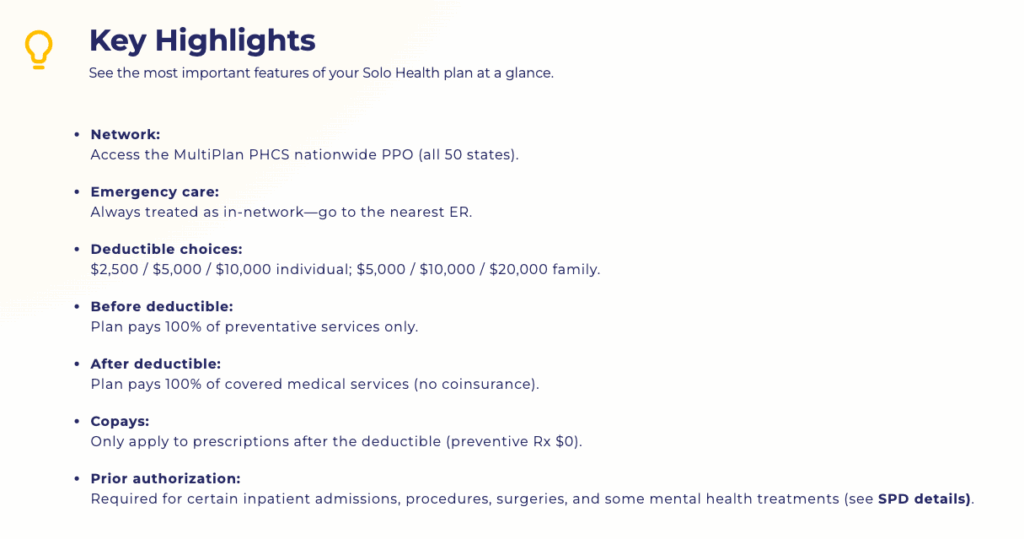

Solo Health Collective utilizes the MultiPlan PHCS (Private Healthcare Systems) network, which is currently one of the largest independent Primary Provider Organizations (PPO) in the United States. This network includes over 1.4 million providers across all 50 states, addressing a common criticism of marketplace plans: the "narrow network" problem.

The collective offers three primary tiers, which depart from traditional insurance nomenclature:

- The V1500 Plan: Features a $1,500 deductible.

- The V2500 Plan: Features a $2,500 deductible and is compatible with Health Savings Accounts (HSAs).

- The V5000 Plan: Features a $5,000 deductible and is also HSA-compatible.

A distinctive feature of these plans is the alignment of the deductible with the out-of-pocket maximum. In traditional ACA plans, a member might encounter a $5,000 deductible followed by 20% coinsurance until they reach an $8,000 or $9,000 out-of-pocket limit. Solo’s structure dictates that once the deductible is met for covered services, the plan pays at 100% for the remainder of the benefit year.

Comparative Financial Data and Tax Implications

Data provided by the collective and verified through market comparisons suggests significant cost variations between the captive model and traditional exchanges.

For a 35-year-old non-smoking freelancer in a state like Illinois, a standard "Gold" marketplace plan might carry a monthly premium of approximately $550 with a $2,000 deductible and a $9,000 out-of-pocket maximum. Under the Solo V5000 plan, that same individual could see a premium of roughly $330 per month. While the deductible is higher at $5,000, the total financial exposure—the sum of 12 months of premiums plus the out-of-pocket maximum—is often $4,000 to $6,000 lower per year in the Solo model.

Furthermore, the tax treatment of these plans provides a critical advantage for the self-employed. Under Section 162(l) of the Internal Revenue Code, self-employed individuals can generally deduct 100% of their health insurance premiums from their adjusted gross income. Because Solo Health Collective requires members to have a Federal Employer Identification Number (EIN), the premiums are structured as a business-related expense, clarifying the path to tax deductibility.

Eligibility Requirements and Medical Underwriting

Unlike the ACA marketplace, Solo Health Collective is not a "guaranteed issue" program. This distinction is central to its ability to maintain lower premiums. Prospective members must undergo a simplified medical underwriting process, which involves a health questionnaire.

The eligibility criteria include:

- Self-Employment Status: Members must be true solopreneurs, freelancers, or contractors.

- EIN Requirement: Applicants must possess a Federal Tax ID (EIN) to verify their status as a business entity.

- Employment Restrictions: Individuals with W2 employees who are eligible for benefits are generally excluded to maintain the "business of one" risk profile.

- Health Status: The plan is designed for generally healthy individuals. While it covers pre-existing conditions once a member is accepted, the initial screening may result in a denial of coverage for those with high-risk, chronic, or terminal illnesses.

Industry analysts note that this "selective" approach is what allows the captive pool to remain financially stable. By excluding the highest-risk individuals—who are typically served by the ACA’s subsidized risk pools—Solo Health Collective can offer lower rates to the "healthy middle" of the freelance workforce.

Concierge Support and the Human Element

A significant trend in modern healthcare is the "concierge" model, which Solo has integrated to replace traditional customer service. Members are assigned access to a support team reachable via text, phone, or email. This team assists with administrative tasks that often cause "billing friction," such as:

- Verifying if a specific specialist is in-network.

- Estimating the cost of a procedure before it occurs.

- Intervening in "balance billing" disputes where a provider attempts to charge more than the negotiated rate.

This service-oriented approach is a response to the "administrative burden" of healthcare, which a 2022 study published in Health Affairs estimated costs the U.S. economy billions in lost productivity annually, particularly for small business owners who lack HR departments.

Broader Implications for the Labor Market

The emergence of models like Solo Health Collective has broader implications for "portable benefits" in the United States. For decades, the American labor market has been "job-locked," a phenomenon where employees remain in corporate positions they wish to leave solely to maintain health insurance for themselves or their families.

As independent health plans become more robust and cost-effective, the barrier to entry for entrepreneurship decreases. Economists suggest that the decoupling of health insurance from traditional employment could lead to increased "labor market fluidity," allowing more skilled workers to transition into specialized consultancy and freelance roles without sacrificing high-quality medical coverage.

However, the reliance on medical underwriting also highlights a growing divide in the freelance world. While healthy solopreneurs can find relief in captive models, those with chronic conditions remain tethered to the ACA marketplace or traditional employment. Solo Health Collective represents a significant step in market segmentation—providing a tailored tool for a specific subset of the workforce while leaving the broader social safety net to handle the most complex medical risks.

Future Outlook

As Solo Health Collective continues to expand, the organization is expected to leverage its growing data set to offer more predictive wellness features. The inclusion of fitness perks, such as FitOn credits, signals a move toward "preventative maintenance" for the workforce. By incentivizing health, the collective aims to lower the frequency of major claims, thereby keeping premiums stable for the entire group.

For the American solopreneur, the availability of a nationwide PPO with transparent pricing represents a departure from the "least bad option" mentality of previous years. As the freelance economy continues to mature, the success of captive insurance models will likely serve as a blueprint for other professional associations seeking to provide institutional-grade benefits to the independent professional.