Solo Health Collective has introduced a specialized health coverage framework designed to address the systemic financial and administrative challenges faced by the growing population of independent contractors and solopreneurs in the United States. Utilizing a captive insurance model, the organization aims to provide a viable alternative to the traditional Affordable Care Act (ACA) marketplace, which many self-employed professionals cite as a primary barrier to sustainable business ownership. This initiative comes at a critical juncture as the "gig economy" continues to expand, with recent labor statistics indicating that over 60 million Americans now engage in some form of independent work.

The Landscape of Independent Workforce Healthcare

For over a decade, the primary vehicle for health insurance among the self-employed has been the individual marketplace established under the ACA. While the marketplace succeeded in providing coverage to millions with pre-existing conditions, it has frequently been criticized by middle-income freelancers who do not qualify for federal subsidies. These individuals often face a "subsidy cliff," where premiums for even basic "Bronze" plans can exceed $500 per month, coupled with deductibles ranging from $7,000 to $9,000.

Industry data suggests that health insurance remains a top-three concern for individuals considering a transition from traditional employment to full-time freelancing. The lack of employer-sponsored group rates often leaves the self-employed at the mercy of volatile individual market pricing. Solo Health Collective’s entry into this space represents a shift toward "community-funded" models that leverage the collective buying power of independent professionals to mirror the benefits typically reserved for large corporate entities.

The Captive Insurance Model: A Strategic Shift

The cornerstone of the Solo Health Collective approach is the captive insurance model. Historically, captive insurance has been a strategy employed by Fortune 500 companies to manage risk. In this arrangement, a group of businesses creates its own insurance company to provide coverage for its members. By doing so, the group avoids the high administrative overhead and profit margins demanded by commercial insurance giants.

Solo Health Collective applies this logic to the "business of one." By pooling thousands of independent consultants, designers, and contractors into a single captive entity, the organization achieves the scale necessary to negotiate better rates and provide more transparent coverage. Unlike traditional insurers, whose fiduciary duty is to shareholders, the captive model focuses on the solvency and benefit of the member collective. This structure allows for a more direct correlation between member health and premium stability, as the "profit" is essentially reinvested into lower costs or better services for the group.

Chronology and Development of the Collective

The roots of this model trace back to 2015 with the founding of Health Business Group (HBG), the parent organization of Solo Health Collective. HBG initially focused on providing healthcare solutions for small to medium-sized enterprises. However, observing a significant gap in the market for individuals who operated without any W-2 employees, the company began developing the Solo framework in early 2021.

The Solo Health Collective plan was officially launched in 2022. Since its inception, the program has undergone several phases of expansion:

- Phase I (2022): Initial rollout focusing on high-earning consultants in the technology and legal sectors.

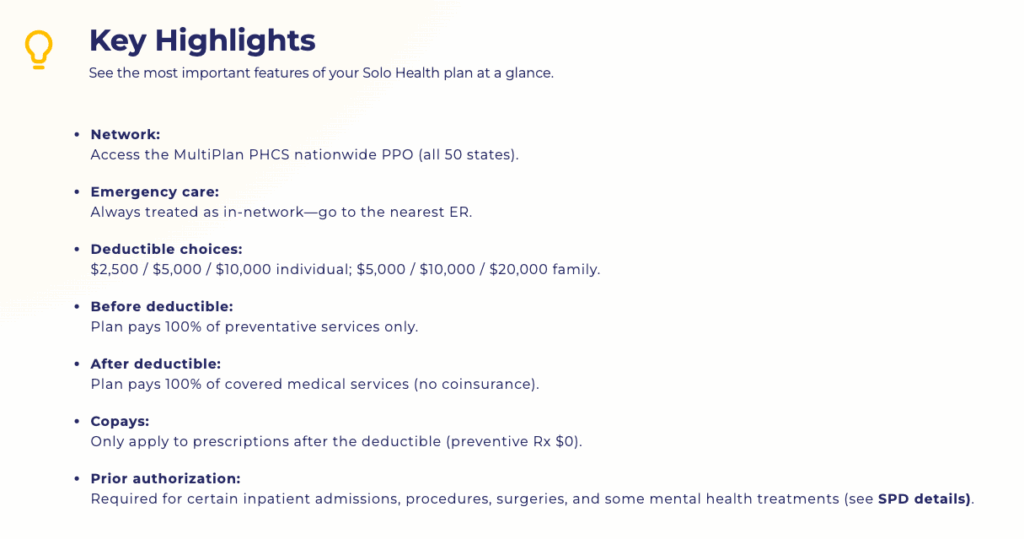

- Phase II (2023): Expansion of the provider network through a strategic partnership with the MultiPlan PHCS network, granting members access to over 1.4 million providers nationwide.

- Phase III (2024): Integration of concierge support services and enhanced pharmacy benefit management to streamline the member experience.

Technical Specifications and Coverage Tiers

The program offers three primary deductible tiers, designed to provide clarity in an industry often criticized for "hidden" costs. A distinguishing feature of the Solo model is the alignment of the deductible with the out-of-pocket maximum. In traditional marketplace plans, a member might pay a $5,000 deductible and still be responsible for 20% coinsurance until reaching an $8,500 out-of-pocket limit. Under the Solo framework, once the deductible is met, the plan covers 100% of all in-network covered services.

The current plan options include:

- V1000: Designed for individuals with higher utilization needs, featuring a $1,000 deductible.

- V2500: A mid-tier option that is compatible with Health Savings Accounts (HSAs).

- V5000: A lower-premium, high-deductible option, also HSA-eligible, targeted at generally healthy individuals seeking catastrophic protection.

All tiers include 100% coverage for preventive care, including annual physicals, immunizations, and standard screenings, regardless of whether the deductible has been met. This emphasis on preventive medicine is a deliberate strategy within the captive model to reduce long-term costs by identifying health issues before they require expensive emergency interventions.

Comparative Financial Analysis

A comparative analysis of the Solo Health Collective versus traditional ACA marketplace plans reveals significant variance in annual expenditure. In a representative case study of a 35-year-old independent contractor in the Midwest, the following data was observed:

- ACA Gold Plan: Monthly premiums averaged $580, with a $2,000 deductible and an $8,700 out-of-pocket maximum. Total potential annual exposure (premiums + max out-of-pocket) reached $15,660.

- Solo V5000 Plan: Monthly premiums averaged $310, with a $5,000 deductible and a $5,000 out-of-pocket maximum. Total potential annual exposure reached $8,720.

This represents a potential annual saving of nearly $7,000. Furthermore, because Solo Health Collective requires members to have a Federal Tax ID (EIN), the premiums are generally treated as a fully deductible business expense under Section 162(l) of the Internal Revenue Code. For a freelancer in the 24% tax bracket, this deduction provides an additional effective subsidy that is not always available or as easily calculated with personal marketplace plans.

Eligibility and Risk Management Protocols

To maintain the lower premium structure of the collective, Solo Health Collective employs a selective enrollment process. This is a departure from the "guaranteed issue" nature of the ACA. Prospective members must meet two primary criteria:

- Professional Status: Applicants must be truly self-employed with no benefit-eligible W-2 employees. The requirement of an EIN serves as a verification mechanism to ensure the collective remains a business-to-business (B2B) entity.

- Health Underwriting: Applicants must complete a medical questionnaire. While the organization states it seeks to be inclusive, the model relies on a "generally healthy" member base to keep the captive fund stable. Individuals with significant, chronic pre-existing conditions requiring high-cost specialty biologics or frequent hospitalizations may be redirected to the ACA marketplace, which is better equipped to subsidize high-risk profiles.

This underwriting process allows the collective to avoid the "adverse selection" trap, where only the sickest individuals join a plan, driving premiums up for everyone. By curating a group of health-conscious professionals, the collective maintains a lower "loss ratio," which translates directly into premium savings for members.

Concierge Support and the Human Element

A common grievance among the self-employed is the administrative burden of navigating healthcare claims. Solo Health Collective has addressed this through a dedicated concierge support system. Unlike the automated "phone trees" typical of major carriers, the Solo concierge team is accessible via text, email, or direct phone lines.

Member feedback and internal data indicate that the concierge team assists in three primary areas:

- Provider Verification: Confirming that specific specialists are within the MultiPlan PHCS network to avoid out-of-network billing surprises.

- Claim Advocacy: Intervening directly with providers or pharmacies if a claim is incorrectly denied or if a member is overcharged at the point of service.

- Prescription Sourcing: Identifying the most cost-effective pharmacies for specific medications.

Broader Impact and Market Implications

The emergence of models like Solo Health Collective suggests a growing fragmentation of the health insurance market. As the traditional "one-size-fits-all" marketplace struggles with rising costs, niche-specific collectives are providing a safety valve for specific demographics.

Economic analysts suggest that if more self-employed individuals migrate to captive models, it could pressure traditional insurers to innovate their offerings for the small business sector. However, there is also the risk that the removal of healthy, middle-income earners from the ACA risk pool could lead to higher premiums for those remaining in the marketplace.

For the individual solopreneur, the implications are largely positive. The ability to enroll outside of the standard "Open Enrollment" period—a feature of the Solo model—provides the flexibility necessary for a career path defined by transition and change. As the workforce continues to decentralize, the demand for portable, transparent, and business-integrated healthcare solutions is expected to grow, positioning Solo Health Collective as a significant participant in the future of American labor benefits.