The landscape of American labor has undergone a radical transformation over the last decade, with millions of professionals transitioning from traditional employment to independent contracting and solopreneurship. However, this shift has exposed a significant structural gap in the United States healthcare system: the lack of affordable, high-quality health insurance for individuals who operate outside the traditional corporate framework. To address this discrepancy, Solo Health Collective has introduced a specialized health plan solution designed exclusively for self-employed individuals, utilizing a captive insurance model to provide group-level benefits to "businesses of one."

For the estimated 64 million Americans participating in the freelance economy, health insurance remains a primary barrier to long-term career sustainability. Traditional options, such as the Affordable Care Act (ACA) Marketplace, often present a binary choice between prohibitively expensive premiums or high-deductible plans that offer limited provider networks. Solo Health Collective aims to disrupt this cycle by pooling the collective risk of healthy independent professionals, effectively creating the buying power typically reserved for large-scale corporations.

The Evolution of Healthcare for the Independent Workforce

The challenge of securing health insurance for the self-employed is not a new phenomenon, but the scale of the issue has intensified alongside the growth of the gig economy. Historically, independent workers have relied on three primary avenues: state or federal exchanges, short-term limited-duration insurance (STLDI), or health-sharing ministries.

Marketplace plans, while providing essential health benefits and guaranteed issue regardless of pre-existing conditions, often struggle with "narrow networks." Many solopreneurs find that their preferred physicians or specialists are excluded from these plans, or that they must navigate complex "Bronze," "Silver," and "Gold" tiers where the out-of-pocket maximums can exceed $9,000 for an individual. Short-term plans, conversely, offer lower premiums but frequently exclude coverage for pre-existing conditions and lack the comprehensive protections required for long-term security.

Solo Health Collective’s entry into the market represents a strategic shift toward the "captive insurance" model. While the parent organization, Health Business Group, has been active since 2015, the Solo-specific initiative was launched in 2022 to refine the application of self-funded health plans for the micro-business sector.

Understanding the Captive Insurance and Self-Funded Model

The technical foundation of Solo Health Collective is the captive insurance model. In a traditional insurance arrangement, a policyholder pays a premium to a commercial insurer. The insurer assumes the risk, manages the claims, and retains any profit. In this model, the insurer’s profitability is often diametrically opposed to the policyholder’s utilization of care, leading to frequent claim denials and opaque pricing.

In contrast, Solo Health Collective utilizes a community-based, self-funded structure. Members of the collective essentially own the captive and fund the health plan. This creates a community of self-employed individuals who collectively share healthcare costs. By removing the high overhead and profit margins associated with major commercial carriers, the collective can redirect funds toward member care and lower premiums.

This structure allows the collective to implement "Reference-Based Pricing" for out-of-network care and negotiate more favorable rates within established networks. For the member, this translates to a transparent cost structure where the primary objective is the maintenance of the collective’s health rather than the maximization of corporate dividends.

Technical Specifications and Plan Architecture

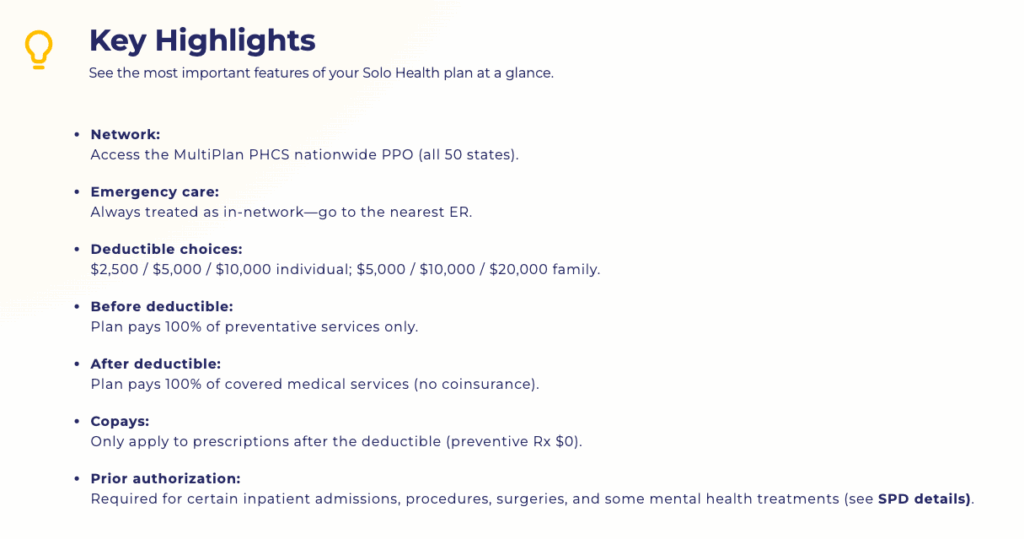

Solo Health Collective offers three distinct tiers of coverage, categorized by deductible levels: $1,500, $2,500, and $5,000. A defining characteristic of these plans is the alignment of the deductible with the out-of-pocket maximum. In traditional insurance, a member might pay a $3,000 deductible and then be responsible for "coinsurance" (e.g., 20% of costs) until reaching an out-of-pocket maximum of $8,000 or more.

Under the Solo model, once a member reaches their chosen deductible, 100% of covered in-network services are paid by the plan. This eliminates the "hidden costs" often associated with medical emergencies. Furthermore, all plans include 100% coverage for preventive care—including annual physicals, immunizations, and screenings—regardless of whether the deductible has been met.

The network infrastructure is supported by the MultiPlan PHCS PPO network, which provides access to over 1.4 million providers across all 50 states. This nationwide portability is a critical feature for "digital nomads" and consultants who travel frequently or maintain residences in multiple states.

Comparative Data: Solo vs. Traditional Marketplace Plans

Financial analysis of current health insurance trends suggests that Solo Health Collective can offer premiums that are 30% to 50% lower than comparable Marketplace coverage for individuals who meet the health qualification standards.

For instance, in a comparative study of a 35-year-old professional in the Midwest, a Marketplace Gold Plan may carry a monthly premium exceeding $550 with a $2,000 deductible and a $9,000 out-of-pocket maximum. In contrast, the Solo V5000 plan for the same individual could cost approximately $260 per month, with a $5,000 deductible that also serves as the out-of-pocket maximum.

In this scenario, the annual premium savings total $3,480. Even if the member were to experience a major medical event and hit the full $5,000 deductible, their total annual expenditure ($3,120 in premiums + $5,000 deductible = $8,120) would still be lower than the maximum exposure under the Marketplace plan ($6,600 in premiums + $9,000 out-of-pocket max = $15,600).

Eligibility, Underwriting, and the EIN Requirement

Unlike ACA-compliant plans, which are required to accept all applicants regardless of health status, Solo Health Collective utilizes a simplified medical underwriting process. Applicants must complete a health questionnaire to determine eligibility. This mechanism is essential to the captive model; by ensuring the collective is comprised of generally healthy individuals, the plan can maintain its lower premium structure.

Industry analysts note that while this excludes individuals with significant pre-existing conditions or chronic illnesses requiring expensive specialty care, it provides a much-needed "middle ground" for the millions of healthy freelancers who currently overpay for insurance to subsidize higher-risk pools in the general marketplace.

Additionally, Solo requires all members to possess a Federal Employer Identification Number (EIN). This requirement serves a dual purpose: it verifies the applicant’s status as a legitimate business entity and ensures that premiums can be treated as a tax-deductible business expense. Under Section 162(l) of the Internal Revenue Code, self-employed individuals can generally deduct 100% of their health insurance premiums from their adjusted gross income, further reducing the effective cost of coverage.

The Concierge Support System as a Service Multiplier

A significant point of differentiation for Solo Health Collective is the integration of human-centric concierge support. Traditional health insurance is often criticized for its "automated" and "adversarial" customer service. Solo provides members with access to a dedicated support team via text, phone, or email.

This team assists with administrative tasks that typically burden the self-employed, such as:

- Verifying if a specific provider is in-network.

- Clarifying the tiered copay structure for prescription medications.

- Resolving billing discrepancies directly with medical offices.

- Navigating the complexities of HSA (Health Savings Account) contributions.

For the 2025 tax year, the V2500 and V5000 plans are HSA-eligible, allowing individuals to contribute up to $4,300 (or $8,550 for families) in pre-tax dollars. The concierge team plays a vital role in educating members on how to leverage these "triple tax-advantaged" accounts to build a long-term medical nest egg.

Broader Implications for Labor Mobility and the Economy

The emergence of specialized health collectives like Solo has broader implications for the U.S. economy, particularly regarding "job lock." Job lock is a phenomenon where employees remain in traditional corporate roles they otherwise would leave, simply to maintain access to employer-sponsored health benefits.

By providing a viable, high-quality alternative to corporate plans, Solo Health Collective facilitates greater labor mobility. When the "healthcare hurdle" is lowered, more professionals feel empowered to launch independent consultancies, contributing to innovation and economic flexibility.

Furthermore, the model encourages proactive health management. By including fitness perks—such as monthly credits for wellness platforms—and covering 100% of preventive care, the collective incentivizes members to maintain their health. This "preventive-first" philosophy reduces the long-term cost of care for the entire community.

Conclusion and Future Outlook

Solo Health Collective represents a maturing of the freelance support ecosystem. As the "business of one" becomes a permanent fixture of the global economy, the demand for sophisticated, community-owned financial and health infrastructures will continue to rise.

While the model is not a universal solution—specifically for those with chronic health conditions who are better served by the guaranteed-issue protections of the ACA—it offers a powerful alternative for the healthy, self-employed professional. By combining the transparency of a community-funded plan with the reach of a nationwide PPO network, Solo Health Collective provides a blueprint for how independent workers can secure their physical and financial well-being without the overhead of a traditional corporation.

As healthcare costs continue to outpace inflation, the success of such collective models will be closely watched by policy analysts and labor advocates alike as a potential solution to one of the most persistent challenges of the modern workforce.