The global freelance economy has reached an unprecedented scale in 2026, with independent contractors now accounting for a significant portion of the professional workforce across North America, Europe, and Asia. As the boundary between traditional employment and independent contracting continues to blur, the infrastructure supporting these workers has undergone a radical transformation. The primary challenge for the modern freelancer has shifted from merely securing work to efficiently managing the complex financial logistics of getting paid. Market data indicates that the choice of a payment platform is no longer a matter of convenience but a strategic business decision that directly impacts net income, professional branding, and cross-border scalability.

The Evolution of Freelance Financial Infrastructure

The trajectory of freelance payments has moved through three distinct eras. The early 2010s were defined by a reliance on legacy banking systems and the early dominance of PayPal. The second era, sparked by the remote work surge of 2020–2023, saw the rise of specialized fintech solutions that prioritized user experience and lower fees. By 2026, the industry has entered a third era characterized by integrated financial ecosystems. Today’s leading platforms do more than move money; they provide automated invoicing, multi-currency treasury management, and real-time cash flow analytics.

According to 2025 year-end industry reports, the average freelancer loses between 2.5% and 5% of their gross revenue to transaction fees and currency conversion markups. In a sector where profit margins are tightly coupled with billable hours, these "silent costs" have driven a mass migration toward platforms that offer transparent pricing and specialized tools for the independent professional.

Comprehensive Business Management: Melio and Stripe

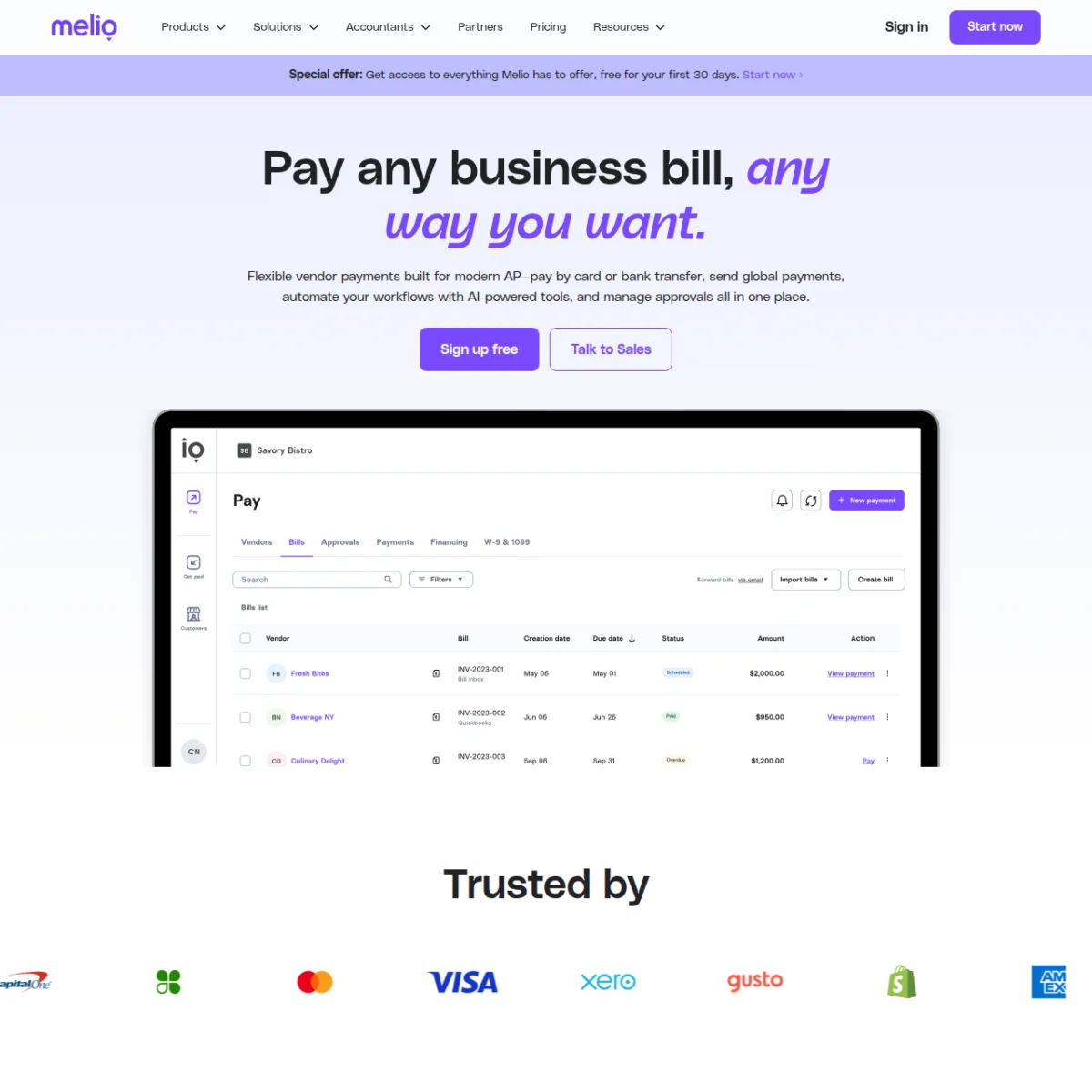

At the forefront of the 2026 payment landscape are platforms that treat freelancing as a structured business enterprise. Melio has emerged as a dominant force by bridging the gap between accounts receivable and accounts payable. Unlike traditional peer-to-peer apps, Melio allows freelancers to manage their entire financial operation from a single dashboard.

Market analysis highlights Melio’s unique value proposition: the ability to send professional invoices while simultaneously managing payments to sub-contractors and vendors. For the established freelancer operating as a Limited Liability Company (LLC) or an S-Corp, the platform’s integration with accounting software like QuickBooks has become a standard requirement. The use of ACH bank transfers, which remain free on the platform, has significantly reduced the overhead for domestic high-value contracts.

Conversely, Stripe remains the gold standard for technical and creative professionals who require a sophisticated digital presence. Stripe’s evolution into a full-scale financial infrastructure provider allows freelancers to implement subscription-based billing models and "buy now, pay later" options for high-ticket consulting packages. Industry data suggests that freelancers using Stripe’s automated reminder systems see a 15% reduction in late payments compared to those using manual invoicing methods.

The Globalization of Independent Work: Wise, Payoneer, and Revolut

As the talent market becomes increasingly borderless, the cost of international transfers has become a primary concern for the "digital nomad" demographic. Traditional wire transfers, once the only reliable method for large international payments, are being phased out in favor of specialized fintech corridors.

Wise (formerly TransferWise) continues to lead the sector in currency transparency. By utilizing the mid-market exchange rate and charging a nominal, upfront fee, Wise has disrupted the traditional banking model that often hid costs within inflated conversion rates. For a freelancer in 2026 billing a client in London while residing in New York, the savings provided by Wise can amount to thousands of dollars annually.

Payoneer remains the critical link for those operating within massive labor marketplaces such as Upwork, Fiverr, and Toptal. Its infrastructure is specifically tuned to the payout cycles of these platforms, offering a "local" bank account experience in multiple jurisdictions. Meanwhile, Revolut Business has gained traction among location-independent professionals who require multi-currency accounts that function like a traditional bank but with the agility of a tech startup. Revolut’s ability to hold and exchange over 30 currencies in real-time provides a hedge against currency volatility, a growing concern in the 2026 global economy.

Domestic Efficiency and the Consumer-Facing Sector

For freelancers whose client base consists of individual consumers or small local businesses, the priority shifts from global reach to "frictionless" domestic transfers. In the United States, Zelle has become a favored tool for established relationships due to its zero-fee structure and integration with major retail banks. Because Zelle moves money directly between bank accounts, it bypasses the "wallet" phase typical of other apps, ensuring immediate liquidity for the freelancer.

However, for less formal engagements or consumer-oriented services—such as personal coaching, photography, or home-based consulting—Venmo Business and Cash App Business have captured a significant market share. These platforms leverage the social familiarity of their parent apps. Data indicates that clients are 20% more likely to pay an invoice immediately if it is delivered through an app they already use for personal transactions. The trade-off, as noted by financial analysts, is the "social" nature of these platforms, which may lack the gravitas required for high-stakes corporate consulting.

Bridging the Physical and Digital Divide: Square

Square occupies a unique niche in the 2026 freelance economy by catering to the "hybrid" professional. This group includes photographers, event planners, and on-site consultants who require the ability to accept payments both in-person and via digital invoices. Square’s hardware ecosystem, which has become ubiquitous in retail, allows freelancers to maintain a consistent brand experience regardless of where the transaction occurs. Its integrated dashboard provides a holistic view of business health, combining point-of-sale data with online billing.

The Economic Impact of Transactional Fees

A critical component of the 2026 freelance strategy is the mitigation of transactional "leakage." To illustrate the impact, a freelancer earning $100,000 per year and using a platform with a 3% flat fee will pay $3,000 annually in processing costs. Over a five-year period, this totals $15,000—capital that could otherwise be diverted to retirement accounts, equipment upgrades, or marketing.

Industry experts emphasize that the "best" payment app is often a combination of tools. The "2026 Payment Stack" typically involves:

- A Primary Processor (Melio or Stripe): For formal business invoicing and domestic ACH.

- An International Specialist (Wise): To handle overseas clients without losing 4-7% to bank spreads.

- A Low-Friction Backup (Zelle or PayPal): To accommodate specific client preferences and ensure no contract is lost due to payment barriers.

Regulatory Context and Compliance

The landscape of 2026 is also defined by stricter regulatory oversight. In the United States, the Internal Revenue Service (IRS) and equivalent global tax authorities have implemented sophisticated reporting requirements for third-party settlement organizations. Most payment apps now automatically generate 1099-K forms for users exceeding minimal thresholds. This shift has forced freelancers to move away from personal accounts toward dedicated business profiles to ensure clean bookkeeping and tax compliance. Platforms that offer robust reporting features have seen higher retention rates as freelancers seek to simplify their year-end tax filings.

Future Outlook: The Convergence of Payments and Banking

Looking toward the latter half of the decade, the trend of "embedded finance" is expected to accelerate. Financial analysts predict that the distinction between a payment app and a business bank account will eventually disappear for the freelance sector. We are already seeing the early stages of this with platforms like Revolut and Square offering lending products and high-yield savings accounts specifically for independent contractors based on their transaction history.

The professional freelancer of 2026 is no longer just a service provider; they are a micro-enterprise. The selection of a payment app has become a reflection of that professionalism. As friction continues to decrease and transparency increases, the advantage will remain with those who treat their payment infrastructure with the same level of scrutiny as their core craft. The right system does not just facilitate a transaction; it secures the financial stability of the independent worker in an increasingly complex global market.